(As per NN 04-2025 Dated 16-01-2025)

Selling old and used vehicles in India involves various tax implications under the Goods and Services Tax (GST) regime. The tax treatment depends on factors such as the period of ownership, Input Tax Credit (ITC) claims, and valuation methods. This blog simplifies the GST and CESS implications for easy understanding.

Key Factors Affecting GST on Sale of Old and Used Vehicles:

When selling an old vehicle, the following factors influence GST and CESS applicability:

- Whether ITC was claimed on the purchase of the vehicle

- The holding period (within or after 5 years of purchase)

- The valuation method applied (transaction value or depreciated value)

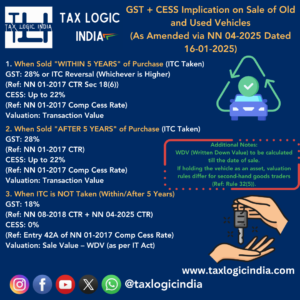

1. When Vehicle is Sold “WITHIN 5 YEARS” of Purchase (ITC Claimed)

Applicability: If the vehicle is sold within 5 years and ITC was taken on purchase.

- GST Rate: 28% (Standard Rate)

- In case of exceptions, rates of 5%, 12%, or 18% may apply.

- Alternatively, ITC reversal as per Rule 43 is applicable (Whichever is higher).

- CESS: Up to 22% (Compensation Cess Rate)

- Valuation: Transaction Value (i.e., the actual selling price of the vehicle)

Example:

A business sells a car after 3 years, and ITC was availed at the time of purchase. The GST rate will be 28%, and cess up to 22% will apply on the transaction value.

2. When Vehicle is Sold “AFTER 5 YEARS” of Purchase (ITC Claimed)

Applicability: If the vehicle is sold after 5 years and ITC was taken on purchase.

- GST Rate: 28% (Standard Rate)

- In case of exceptions, rates of 5%, 12%, or 18% may apply.

- CESS: Up to 22% (Compensation Cess Rate)

- Valuation: Transaction Value (actual selling price)

Example:

A company sells a commercial vehicle after 6 years, having claimed ITC. The sale attracts 28% GST and 22% cess on the selling price.

3. When ITC is NOT Taken (Sold Within/After 5 Years)

Applicability: If ITC was not availed at the time of purchase.

- GST Rate: 18% (As per NN 08-2018 & NN 04-2025)

- CESS: 0% (No Compensation Cess applicable)

- Valuation:

- Sale Value minus Written Down Value (WDV) as per Income Tax Act

Example:

A small business sells an old vehicle where ITC was not claimed at purchase. The GST rate applicable is 18%, and no cess is levied.

Understanding Valuation Methods:

The method of valuation for GST depends on the accounting treatment:

- For businesses holding vehicles as assets in books:

- The transaction value (selling price) is considered for GST purposes.

- For businesses dealing in second-hand vehicle sales:

- Rule 32(5) of CGST Rules applies, where margin schemes may be used for valuation.

- For ITC not claimed cases:

- Sale price minus WDV (depreciated value) is taken for tax calculation.

Comparison Table for Easy Understanding:

| Condition | GST Applicability | CESS Applicability | Valuation Method |

|---|---|---|---|

| ITC Claimed, Sale Within 5 Years | 28% or ITC Reversal (Higher) | Up to 22% | Transaction Value |

| ITC Claimed, Sale After 5 Years | 28% | Up to 22% | Transaction Value |

| ITC Not Claimed | 18% | 0% | Sale Value – WDV |

Key Takeaways:

- If ITC is claimed, higher GST rates and cess apply.

- If ITC is not claimed, a concessional GST rate of 18% is applicable.

- For vehicles treated as business assets, transaction value is used for taxation.

- No cess is applicable if ITC was not claimed.

Frequently Asked Questions (FAQs):

Q1: What is the GST rate if an individual sells their personal car?

A: If the sale is made by an individual (not registered under GST), no GST is applicable.

Q2: Can I claim ITC on a personal vehicle used for business purposes?

A: ITC is only allowed if the vehicle is used for eligible business activities (e.g., transportation services).

Q3: How is cess calculated for luxury cars?

A: Cess is applicable up to 22% based on the vehicle type and value, as per NN 01-2017 Comp Cess Rate.

Q4: What happens if I sell a vehicle purchased before the GST era?

A: Pre-GST vehicles may be subject to valuation adjustments, but GST still applies on the sale.

Conclusion:

Understanding the GST and CESS implications on the sale of old and used vehicles is crucial for compliance and avoiding unnecessary tax burdens. Businesses should assess whether ITC was claimed and follow the correct valuation method to ensure accurate tax calculations.

For professional advice and assistance with GST compliance, consult an expert.

For More Information & Updates:

Tax Logic India

🌐 taxlogicindia.com

📞 6381139685

👉 bit.ly/4fnYxx6 (Follow for more updates)